PEA Demonstrates Robust Economics and Optionality to Produce Nickel for the Electric Vehicle or Stainless Steel Markets

Road Town, Tortola, British Virgin Islands--(Newsfile Corp. - February 4, 2021) - Talon Metals Corp. (TSX: TLO) ("Talon" or the "Company") is pleased to announce that it has completed an updated Preliminary Economic Assessment (the "February 2021 PEA") in respect of the Tamarack Nickel-Copper Cobalt Project (the "Tamarack Nickel Project"). Talon currently has the right to acquire up to a 60% ownership interest in the Tamarack Nickel Project upon the satisfaction of certain terms and conditions1.

Highlights

- The February 2021 PEA provides economics for three considered scenarios:

- nickel sulphates used for the electric vehicle (EV) market ("Nickel Sulphate Scenario");

- nickel concentrates used to produce refined nickel powders for the electric vehicle (EV) market ("Nickel Powder Scenario"); and

- nickel concentrates used for the traditional stainless steel market ("Nickel Concentrate Scenario");

- After-tax NPV's of:

- US$569 million (after-tax IRR of 31.9%) (Nickel Sulphate Scenario);

- US$567 million (after-tax IRR of 48.3%) (Nickel Powder Scenario); and

- US$520 million (after-tax IRR of 45.6%) (Nickel Concentrate Scenario),

using base case metal price assumptions of $8.00/lb nickel and $3.00/lb copper and a discount rate of 7%;

- At incentive metal prices of $9.50/lb nickel and $3.50/lb copper, the after-tax NPV's increase to:

- US$769 million (after-tax IRR of 38.6%) (Nickel Sulphate Scenario);

- US$744 million (after-tax IRR of 57.7%) (Nickel Powder Scenario); and

- US$695 million (after-tax IRR of 55.1%) (Nickel Concentrate Scenario).

- The above-noted economics exclude the Company's recent positive drilling results both within the Tamarack Nickel Project's current resource area (see the Company's press releases dated January 12, 2021 and January 26, 2021) and approximately 350 meters up-dip to the north-east of the Tamarack Nickel Project's current resource area (i.e., drill results form the area known as CGO East, as discussed in the Company's press releases dated September 16, 2020 and November 2, 2020).

- Low C1 Costs2 and All-in Sustaining Cost (net of by-product revenue) for all three contemplated scenarios, including a C1 Cost of $2.05/lb nickel and an All-in Sustaining Cost of $3.01/lb nickel under the scenario of selling nickel concentrates to the stainless-steel market (Nickel Concentrate Scenario);

- Pre-tax payback period ranging from 1.4 to 1.8 years and after-tax payback period ranging from 1.5 to 2.1 years;

- EBITDA margins ranging from 64% to 68%;

- Overall tonnage included in the mine plan has increased by 119% from 4.9 million tonnes[3] to 10.8 million tonnes; and

- Processing rate has increased 80% from 2,000 tonnes per day to 3,600 tonnes per day.

"The 96% increase in the after-tax NPV from US$291 million to US$569 million excludes drilling results announced since September 2020, as these drilling results are either outside of the Tamarack Nickel Project's resource area and/or assays are still pending. Our focus continues to be a systematic approach of resource expansion. The Talon team has successfully reduced exploration costs to very low levels, while predicting mineralization with great accuracy using both borehole and surface electromagnetic surveys (geophysics). Carefully designed drill holes are intercepted with precision. The utility of data collected from each drill hole is then maximized through detailed logging procedures, test programs and continual mine modelling," said Henri van Rooyen, CEO of Talon. "Our end game is producing low cost, Green NickelTM during a predicted period of unprecedented nickel shortages, whether it is to supply the electric vehicle (EV) or stainless steel market."

"Today's announcement of the updated Preliminary Economic Assessment, which demonstrates strong economics across a number of scenarios, is a significant milestone for our Company", said Sean Werger, President of Talon. "Having said that, there is much more to come. Indeed, this is evidenced by the fact that today's economics exclude the tremendous drilling success we have recently announced both within our current resource area (where we have announced extensions of massive sulphide mineralization) and approximately 1/3 of a kilometer north-east and up-dip of our resource area (where we have announced shallow, sheet-like mineralization). We are pleased to report that we now have three drill rigs running at site, so shareholders should expect plenty of drilling news over the coming days, weeks and months. With approximately C$15.4 million currently in the bank, we are well equipped to progress our strategy of growing the resource further and getting ready for feasibility studies."

"This updated Preliminary Economic Assessment (PEA) illustrates a high after-tax IRR, low All-in Sustaining Cost, low capital intensity, a modest initial capital investment, and a quick payback. These metrics are the hallmarks of a high quality mining project. The PEA also demonstrates that the Tamarack Nickel Project has the optionality to produce (1) nickel sulphates for the electric vehicle (EV) market; (2) nickel concentrates to be used for refined nickel powders also for the electric vehicle (EV) market; or (3) nickel concentrates for the traditional stainless steel market, and that all three contemplated scenarios have robust economics. None of the three scenarios include a nickel price premium for ESG-sensitive nickel production which we refer to as Green NickelTM", said Vince Conte, CFO of Talon. "With additional drilling and engineering in 2021, we are aiming to further increase the NPV of the Tamarack Nickel Project."

____________________

1 All amounts are presented on a 100% ownership basis and all dollar amounts are expressed in United States dollars unless indicated otherwise.

2 C1 cost includes value of metal claimed by smelter (metal units, treatment charges and refining charges), insurance, losses and transportation costs, less the value of by-products such as copper and cobalt. C1 cost is not an IFRS (International Financial Reporting Standards) measure and, although it is calculated according to accepted industry practice, the C1 cost may not be directly comparable to calculations carried out by other companies.

3 See the technical report entitled "NI 43-101 Technical Report Updated Preliminary Economic Assessment (PEA) of the Tamarack North Project - Tamarack, Minnesota" with an effective date of March 12, 2020 (the "March 2020 PEA") for comparisons in this news release. The March 2020 PEA is available under the Company's issuer profile on SEDAR (www.sedar.com) or on the Company's website (www.talonmetals.com).

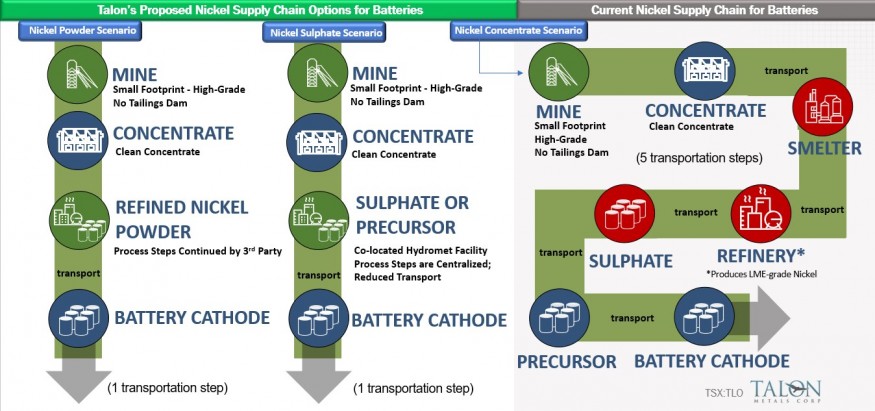

Product Optionality to Meet the Needs of the Electric Vehicle (EV) Battery Supply Chain or Traditional Nickel Smelters

The February 2021 PEA has modelled three scenarios, as follows:

| Scenario | Description | |

| 1 | Nickel Powder Scenario | Nickel concentrates produced at site and thereafter used to produce refined nickel powder by a third party for the EV market |

| 2 | Nickel Sulphate Scenario | Nickel sulphates produced at site for the EV market |

| 3 | Nickel Concentrate Scenario | Nickel concentrates produced at site and sold to a smelter, which produces LME grade nickel primarily for the stainless steel market |

The following chart illustrates the three separate potential offtake options that Talon is pursuing. All three options are economic, which enhances the strategic optionality of the Tamarack Nickel Project.

Figure 1: Talon's Proposed Nickel Supply Chain Options for Batteries Compared to the Current (Inefficient) Nickel Supply Chain for Batteries

Figure 1: Talon's Proposed Nickel Supply Chain Options for Batteries Compared to the Current (Inefficient) Nickel Supply Chain for Batteries

Comparison of the March 2020 PEA to Scenarios Modelled in the February 2021 PEA

The following table provides the key metrics of the three scenarios modelled in the February 2021 PEA, with the results from the historical March 2020 PEA provided for comparative purposes.

Table 1: Key Metrics of February 2021 PEA compared to March 2020 PEA

| All amounts in United States dollars |

March 2020 PEA(1) | February 2021 PEA | ||

| NICKEL POWDER SCENARIO | NICKEL SULPHATE SCENARIO | NICKEL CONCENTRATE SCENARIO | ||

| After-Tax NPV(2), (3) | $291 million | $567 million | $569 million | $520 million |

| After-Tax IRR(2) | 36.0% | 48.3% | 31.9% | 45.6% |

| Initial CAPEX and Working Capital | $219 million | $316 million | $553 million | $316 million |

| Payback Period, pre-tax(4) | 2.3 years | 1.4 years | 1.8 years | 1.4 years |

| Payback Period, after-tax(4) | 2.5 years | 1.5 years | 2.1 years | 1.6 years |

(1) The March 2020 PEA is available under the Company's issuer profile on SEDAR (www.sedar.com) or on the Company's website (www.talonmetals.com). The March 2020 PEA was based on a nickel concentrate scenario.

(2) Metal prices of $8.00/lb Ni, $3.00/lb Cu, $25.00/lb Co, $1,000/oz Pt, $1,000/oz Pd and $1,300/oz Au. The same metal prices have been used in both the March 2020 PEA and the February 2021 PEA.

(3) Discount rate of 7%. NPV calculated from the start of construction.

(4) From the start of production.

Figure 2: After-tax NPV, Initial CAPEX and After-tax IRR for the Nickel Powder, the Nickel Sulphate and Nickel Concentrate Scenarios, including results from the March 2020 PEA for comparative purposes

Figure 2: After-tax NPV, Initial CAPEX and After-tax IRR for the Nickel Powder, the Nickel Sulphate and Nickel Concentrate Scenarios, including results from the March 2020 PEA for comparative purposes

At current metal prices and incentive metal prices, the after-tax NPV and after-tax IRR are as follows:

Table 2: After-tax NPV and After-tax IRR of February 2021 PEA using Current Metal Prices and Incentive Metal Prices

| All amounts in United States dollars |

February 2021 PEA | ||

| NICKEL POWDER SCENARIO | NICKEL SULPHATE SCENARIO | NICKEL CONCENTRATE SCENARIO | |

| Current Metal Prices of $7.98/lb Ni and $3.55/lb Cu | |||

| After-Tax NPV(1), (2) | $602 million | $597 million | $565 million |

| After-Tax IRR(1) | 50.1% | 32.9% | 48.0% |

| Incentive Metal Prices of $9.50/lb Ni and $3.50/lb Cu | |||

| After-Tax NPV(3), (2) | $744 million | $769 million | $695 million |

| After-Tax IRR(3) | 57.7% | 38.6% | 55.1% |

(1) Metal prices of $7.98/lb Ni, $3.55/lb Cu, $19.97/lb Co, $1,107/oz Pt, $2,348/oz Pd and $1,834/oz Au as of February 3, 2021

(2) Discount rate of 7%. NPV calculated from the start of construction.

(3) Metal prices of $9.50/lb Ni, $3.50/lb Cu, $30.00/lb Co, $1,000/oz Pt, $1,000/oz Pd and $1,300/oz Au. Incentive price is an estimated price believed to be required to incentivize new mines to be constructed. Selected incentive price based on research, however may be higher or lower dependent on numerous factors such as: inflation, future volume of demand for nickel, required return on capital and cost profile (both CAPEX and OPEX) of new projects that potentially could be constructed to meet a supply shortfall among other factors. Incentive price represents a possible price during periods of nickel demand growth such as due to the projected growth in the EV market.

Additional metrics of the February 2021 PEA compared to the March 2020 PEA are included in the following table:

Table 3: Additional Metrics of February 2021 PEA compared to March 2020 PEA

| All amounts in United States dollars |

March 2020 PEA | February 2021 PEA | ||

| NICKEL POWDER SCENARIO | NICKEL SULPHATE SCENARIO | NICKEL CONCENTRATE SCENARIO | ||

| Mine Plan Tonnage | 4.9 million | 10.8 million | 10.8 million | 10.8 million |

| Mill Treatment Capacity | 2,000 tpd | 3,600 tpd | 3,600 tpd | 3,600 tpd |

| Mine Life from Start of Production | 8 years | 9 years | 9 years | 9 years |

| Ni Tonnes in situ | 103,000 | 144,000 | 144,000 | 144,000 |

| NiEq Grade of Mill Feed(1) | 2.82% | 1.85% | 1.85% | 1.85% |

| Ni Grade of Mill Feed | 2.10% | 1.34% | 1.34% | 1.34% |

| Cu Grade of Mill Feed | 1.06% | 0.76% | 0.76% | 0.76% |

| Ni Recovery | 83.4%(2) | 82.1%(2) | 78.0%(3) | 82.1%(2) |

| Total Cu Recovery | 94.4%(4) | 86.9%(4) | 84.5%(5) | 86.9%(4) |

| Recovered Metal - Ni tonnes - Cu tonnes |

86,000 48,900 |

118,000 70,700 |

112,000 68,600 |

118,000 70,700 |

| Ni Concentrate Grades | 13.30% Ni, 1.13% Cu |

10.57% Ni, 0.95% Cu |

n/a | 10.57% Ni, 0.95% Cu |

| Cu Concentrate Grade | 27.60% Cu, 2.91 g/t Au |

27.04% Cu, 5.02 g/t Au |

26.45% Cu 4.3 g/t Au |

27.04% Cu, 5.02 g/t Au |

| Tonnes of Product Produced over Life of Mine (DMT) - Nickel Concentrate - Copper Concentrate - Nickel Sulphate |

647,000 151,000 n/a |

1,117,000 222,000 n/a |

n/a 260,000 505,000 |

1,117,000 222,000 n/a |

| Initial CAPEX and Working Capital | $219 million | $316 million | $553 million | $316 million |

| Total CAPEX (including Sustaining CAPEX) | $259 million | $395 million | $646 million | $395 million |

| Capital Intensity (Total CAPEX per Annual Tonne of Nickel-equivalent Production)(6) | $21,000 | $23,000 | $40,000 | $23,000 |

| EBITDA Margin | 60% | 68% | 64% | 64% |

| Pre-tax Cash Flow (EBIT) Margin | 43% | 50% | 41% | 46% |

| Revenue Split Ni/Cu/Other(7) | 77%/19%/4% | 76%/20%/4% | 79%/15%/6% | 74%/20%/6% |

| Ni Sulphate Premium(8) | n/a | n/a | $1.25/lb of Ni | n/a |

(1) NiEq grade based on base case metal prices of $8.00/lb Ni, $3.00/lb Cu, $25.00/lb Co, $1,000/oz Pt, $1,000/oz Pd and $1,300/oz Au using the following formula: NiEq% = Ni%+ Cu% x $3.00/$8.00 + Co% x $25.00/$8.00 + Pt [g/t]/31.103 x $1,000/$8.00/22.04 + Pd [g/t]/31.103 x $1,000/$8.00/22.04 + Au [g/t]/31.103 x $1,300/$8.00/22.04. No adjustments were made for recovery or payability.

(2) To nickel concentrate

(3) To nickel sulphate

(4) To nickel and copper concentrate

(5) To copper concentrate

(6) Calculated as total CAPEX divided by average annual NiEq production during years 2 through 8.

(7) Other includes cobalt, platinum, palladium and gold

(8) Relative to LME Ni price

Figure 3: Long-Section (looking west) of the February 2021 PEA Conceptual Mine Plan Development and Stopes in Relation to the Mineral Domains

Figure 3: Long-Section (looking west) of the February 2021 PEA Conceptual Mine Plan Development and Stopes in Relation to the Mineral Domains

Updated Mineral Resource Estimate

The mineral resource estimate for the Tamarack North Project has been estimated in conformity with November 2019 CIM "Estimation of Mineral Resource and Mineral Reserves Best Practice" guidelines.

Mineral resources are not mineral reserves and do not necessarily demonstrate economic viability. There is no certainty that all or any part of this mineral resource will be converted into a mineral reserve.

This mineral resource estimate has been prepared by Mr. Brian Thomas (P.Geo), Senior Resource Geologist of Golder Associates Limited (Golder). The effective date of the mineral resource estimate is January 8, 2021. Mr. Brian Thomas is an independent "Qualified Person" as defined in National Instrument 43-101: Standards of Disclosure for Mineral Projects ("NI 43-101").

The mineral resource estimate has four domains:

- Upper Semi-Massive Sulphide Unit ("USMSU")

- Lower Semi-Massive Sulphide Unit ("LSMSU")

- Massive Sulphide Unit ("MSU")

- 138 Zone ("138")

The updated mineral resource estimate is based on a block modeling methodology consisting of 5m x 5m x 5m blocks for the USMSU, LSMSU and 138 Domains and 2.5m x 2.5m x 2.5m blocks for the MSU. All Domains were "unfolded" and had top cuts applied to restrict outlier values (Pt, Pd and Au). Resources were estimated using either Ordinary Kriged or Inverse Distance methodologies to interpolate grades (Ni, Cu, Co, Pt, Pd and Au) from 1.5m composited drill hole samples. Density values were based on specific gravity measurements and regression formulas where absent. The mineral resource estimate is reported at a 0.5% nickel cut-off and was determined to have reasonable prospects for mining.

Table 4: Tamarack North Mineral Resource Estimate: Effective January 8, 2021

| Domain | Classification | %Ni Cut-Off |

Tonnes (000) |

Ni (%) |

Cu (%) |

Co (%) |

Pt (g/t) |

Pd (g/t) |

Au (g/t) |

NiEq (%) |

| USMSU | Indicated Resource | 0.5 | 1,462 | 1.32 | 0.78 | 0.04 | 0.17 | 0.11 | 0.11 | 1.81 |

| LSMSU | Indicated Resource | 0.5 | 2,340 | 2.08 | 1.10 | 0.05 | 0.55 | 0.34 | 0.25 | 2.87 |

| MSU | Indicated Resource | 0.5 | 124 | 5.72 | 2.36 | 0.12 | 0.60 | 0.46 | 0.23 | 7.23 |

| Total | Indicated Resource | 0.5 | 3,926 | 1.91 | 1.02 | 0.05 | 0.41 | 0.26 | 0.20 | 2.62 |

| USMSU | Inferred Resource | 0.5 | 2,652 | 0.76 | 0.47 | 0.02 | 0.25 | 0.14 | 0.12 | 1.10 |

| LSMSU | Inferred Resource | 0.5 | 115 | 0.86 | 0.51 | 0.02 | 0.57 | 0.36 | 0.24 | 1.34 |

| MSU | Inferred Resource | 0.5 | 443 | 5.93 | 2.52 | 0.12 | 0.70 | 0.52 | 0.26 | 7.53 |

| 138 | Inferred Resource | 0.5 | 3,953 | 0.82 | 0.63 | 0.02 | 0.21 | 0.12 | 0.14 | 1.21 |

| Total | Inferred Resource | 0.5 | 7,163 | 1.11 | 0.68 | 0.03 | 0.26 | 0.16 | 0.14 | 1.57 |

All resources reported at a 0.5% Ni cut-off.

No modifying factors have been applied to the estimates.

Tonnage estimates are rounded to the nearest 1,000 tonnes.

Metallurgical recovery factored into the reporting cut-off.

NiEq grade based on base case metal prices of $8.00/lb Ni, $3.00/lb Cu, $25.00/lb Co, $1,000/oz Pt, $1,000/oz Pd and $1,300/oz Au using the following formula: NiEq% = Ni%+ Cu% x $3.00/$8.00 + Co% x $25.00/$8.00 + Pt [g/t]/31.103 x $1,000/$8.00/22.04 + Pd [g/t]/31.103 x $1,000/$8.00/22.04 + Au [g/t]/31.103 x $1,300/$8.00/22.04. No adjustments were made for recovery or payability.

Table 5: Tamarack North Mineral Resource Estimate In Situ Metal (Undiluted)

| Classification | Tonnes of Ni In Situ |

Tonnes of NiEq(1) In Situ | Million lbs of Ni In Situ |

Million lbs of NiEq(1) In Situ |

| Indicated Resource | 74,987 | 102,795 | 165 | 227 |

| Inferred Resource | 79,509 | 112,352 | 175 | 248 |

(1) NiEq based on base case metal prices of $8.00/lb Ni, $3.00/lb Cu, $25.00/lb Co, $1,000/oz Pt, $1,000/oz Pd and $1,300/oz Au. No adjustments were made for recovery or payability.

February 2021 PEA Results

The basis of design of the February 2021 PEA, which was completed on the USMSU, LSMSU, MSU and the 138 Domains, is summarized in Table 6 below. The February 2021 PEA is preliminary in nature and includes inferred mineral resources. Inferred mineral resources are considered too speculative geologically to have economic considerations applied to them that would enable them to be categorized as mineral reserves. There is no certainty that the February 2021 PEA will be realized.

Table 6: Basis of Design: February 2021 PEA(1)

| No | Parameter | Description |

| 1 | Approach and Mandate | Implement best available technologies to protect the environment, while creating a catalyst for establishing a long-term, sustainable industry. |

| 2 | Mine Access Method | Decline ramp from surface with a road header |

| 3 | Mine Methods | Long-hole stoping and drift and fill. Lateral development completed primarily with a road header. |

| 4 | Mine Operations | Contract labour mining with owner equipment supply. Mobile equipment is purchased. |

| 5 | Material Flow | Vertical conveyor (primary) with some truck haulage |

| 6 | Mill Feed | 10.8 Mt milled at 1.34% Ni, 0.76% Cu, 0.035% Co, 0.27 Pt g/t, 0.17 Pd g/t and 0.14 Au g/t equating to 1.85% NiEq(3). |

| 7 | Type of Metallurgical Process | Bulk rougher flotation followed by cleaning of the bulk rougher concentrate and Cu/Ni separation. In the case of the Nickel Sulphate Scenario, additional hydrometallurgical processing. Hydrometallurgical refinery (Nickel Sulphate Scenario only): Pressure oxidation leach, neutralization, Cu recovery, solvent extraction, nickel sulphate and cobalt sulphide production. |

| 8 | Separation of Tailings | Bulk rougher tailings are treated in a desulphurization stage to produce a low-mass high sulphur stream and high-mass low sulphur tailings. |

| 9 | Backfill | Cemented paste backfill utilizing all high sulphur tailings generated and low sulphur tailings. |

| 10 | Co-disposed Filtered Tailings Facility ("CFTF") | Filtered low sulphur tailings (at 85% solids) co-disposed with waste rock in a lined surface facility. The liner system of the facility will consist of a composite liner overlain by a drainage layer. Contact water from the facility will be collected in perimeter ditches and subsequently treated. Upon closure, the CFTF will be encapsulated by a composite cover. The Company is studying the potential for sequestrating CO2 within the CFTF. |

| 11 | Mill Treatment Capacity | 3,600 t/d for concentrator/mill 475 t/d for hydrometallurgical refinery in the Nickel Sulphate Scenario. |

| 12 | Mine Life | 9 years (excluding construction period). |

| 13 | Existing Project Infrastructure | Paved highway, grid power, railway line across site, port. |

| 14 | Sustainable Development | The Company is studying the potential of establishing a solar garden to generate energy during and post mining. |

(1) See February 2021 PEA for further details in respect of this table to be published under the Company's issuer profile on SEDAR (www.sedar.com) within 45 days of this news release.

(2) Resources included in the Life of Mine Mined Tonnes were evaluated by calculating the NSR, using the following metal prices: $8.00/lb Ni and $3.00/lb Cu. Revenue from Co, Au, Pt and Pd was not considered to be conservative. Relevant functions were applied such as metal recovery curves, smelting and refining terms, transportation costs and state royalties as applicable. The calculated NSR was then compared to the operating cost per tonne to determine inclusion or exclusion of resource into the mine plan based on value addition or destruction.

(3) NiEq% = Ni%+ Cu% x $3.00/$8.00 + Co% x $25.00/$8.00 + Pt [g/t]/31.103 x $1,000/$8.00/22.04 + Pd [g/t]/31.103 x $1,000/$8.00/22.04 + Au [g/t]/31.103 x $1,300/$8.00/22.04. No adjustments were made for recovery or payability.

Capital and Operating Costs

Capital costs for the Tamarack North Project were estimated by DRA Americas Inc. for the mine, process and surface facilities, by Paterson & Cooke Canada Inc. for the paste backfill and by SLR Consulting (Canada) Ltd. for the CFTF. All cost estimates have been forecast in US dollars using constant, fourth quarter 2020 dollars, (i.e. in "real" dollars), without provision for inflation or escalation, and are subject to change if new information is received or circumstances change.

Mine capital costs were mostly based on budgetary quotes from vendors and/or guidance from contractors. The remaining process and surface infrastructure, as well as some minor mine infrastructure costs, were based on consultant database information. Mine, process and surface operating costs are based on a combination of both budgetary quotes and consultant database information. Various operating parameters are based on historical information or are based on vendor support.

Capital Costs

The total estimated capital cost for each of the Nickel Powder Scenario or the Nickel Concentrate Scenario is US$394.99 million of which US$315.80 million is the initial cost required during the first three years, including the first production year. The total estimated capital cost of the Nickel Sulphate Scenario is US$646.44 million, of which US$552.61 million is the initial cost required during the first three years, including the first production year. The amounts include indirect costs and contingency.

Table 7: Capital Costs

| US$ millions | Nickel Powder Scenario or Nickel Concentrate Scenario |

Nickel Sulphate Scenario | ||||

| Area | Initial Cost (US$M) |

Sustaining Cost (US$M) | Total Cost (US$M) |

Initial Cost (US$M) |

Sustaining Cost (US$M) | Total Cost (US$M) |

| Mine | $130.15 | $70.32 | $200.47 | $130.15 | $70.32 | $200.47 |

| Process and Surface Facilities | $167.51 | $22.01 | $189.51 | $390.56 | $50.41 | $440.97 |

| Closure Costs other than CFTF | - | $10.00 | $10.00 | - | $10.00 | $10.00 |

| Salvage Value of Mill | - | ($5.00) | ($5.00) | - | ($5.00) | ($5.00) |

| Sub Total | $297.66 | $97.33 | $394.99 | $520.71 | $125.73 | $646.44 |

| Working Capital | $18.15 | ($18.15) | - | $31.90 | ($31.90) | - |

| Total | $315.80 | $79.18 | $394.99 | $552.61 | $93.83 | $646.44 |

Operating Costs

The average operating cost for the 9 year mine life is US$48.15/tonne of mill feed in the Nickel Powder Scenario, US$75.99/tonne of mill feed in the Nickel Sulphate Scenario and US$56.54/tonne of mill feed in the Nickel Concentrate Scenario, and detailed in the following table.

Table 8: Operating Cost per Tonne of Mill Feed

| Cost Category | Operating Cost (US$/t of Mill Feed) | ||

| Nickel Powder Scenario | Nickel Sulphate Scenario | Nickel Concentrate Scenario | |

| Mining | $27.49 | $27.49 | $27.49 |

| Processing (milling/concentrating) | $14.25 | $14.25 | $14.25 |

| Hydrometallurgical Refining | - | $26.68 | - |

| Product Handling, Transportation, Losses, and Insurance | $1.90 | $2.22 | $10.29 |

| Co-disposed Filtered Tailings Facility (CFTF) | $0.75 | $0.75 | $0.75 |

| General & Administrative | $3.76 | $4.60 | $3.76 |

| Total OPEX | $48.15 | $75.99 | $56.54 |

Mining costs include variable and allocated fixed operational costs only. All mobile and other equipment, as well as all development costs, are included in initial and sustaining capital costs.

A review of the underground mine plan was completed with the objective of reducing mine capital and operating costs and accelerating time to first production. Several opportunities were evaluated and incorporated into the February 2021 PEA. These are summarized in the following table.

Table 9: February 2021 PEA Mine Design Updates Compared to March 2020 PEA

| March 2020 PEA | February 2021 PEA | |

| Primary Access | Shaft | Decline |

| Primary Development Method | Drill / Blast | Road Header |

| Longhole Stope Sizes | 7.5m W x 15m H x 15m L | 15m W x 25m H x 30m L |

| Drift and Fill Size | 3.0m W x 3.0m H | 6.5m W x 5.0m H |

| Mobile Equipment | Leased (opex) | Purchased (capex/sustaining) |

| Material Handling | Hoisting (Skips) | Vertical Conveyor |

| Main Infrastructure | Underground | Surface |

The overall mining cost is US$27.49/t of mill feed and consists of direct mining costs, backfill, cross cut development, material flow, truck haulage, services, management, engineering and supervision.

The breakdown of tonnes milled and cost by mining method is shown in the following table:

Table 10: Mining Operating Cost by Mining Method

| Mining Method | Tonnes Mined | Percentage of Total | Mine Operating Cost (US$/t of mill feed) |

| Drift & Fill | 779,382 | 7.2% | $39.95 |

| Long hole Stoping | 8,456,397 | 78.6% | $22.86 |

| Ore Development | 1,523,017 | 14.2% | $46.88 |

| Totals | 10,758,796 | 100.0% | $27.49 (weighted average) |

Processing costs include variable and allocated fixed costs related to processing of mineralized material, from milling through to concentrate or sulphate production (depending upon the selected scenario).

Product handling, transportation losses and insurance are higher for the Nickel Concentrate Scenario, as the nickel concentrate is sold on a Cost Insured Freight ("CIF") basis. In contrast, in the Nickel Powder Scenario, the nickel concentrate is sold on a Free on Board ("FOB") basis at the mine gate. In the Nickel Sulphate Scenario, nickel sulphates are sold on an FOB basis. In all scenarios, the copper concentrate is sold on a CIF basis.

The cost of the CFTF consists of all variable and allocated fixed costs from the mill through to mine closure.

C1 Cost and All-in Sustaining Cost ("AISC")

A) Nickel Powder Scenario

No benchmark has been set for expressing C1 cash cost or AISC for selling nickel powders to the EV industry in large quantities.

To be consistent with the nickel-to-stainless steel industry best practices, the following methodology has been used:

C1 Cash Cost: The cash cost of producing a pound of nickel in concentrate sold FOB at the mine gate less all by-product credits is shown in the following table:

Table 11: C1 Cash Cost of the Nickel Powder Scenario

| Cost | $/lb Ni in Concentrate |

| On-site Cash Costs | $1.91 |

| Off-site Costs of By-products | $0.19 |

| Less: By-product Revenue | ($2.01) |

| Net Cost of Producing Nickel in Concentrate at the Mine Gate | $0.08* |

*Does not total due to rounding

Nickel concentrates need to be refined to produce nickel powder for the EV industry, which will require additional capital and operating costs: For instance, if it costs $1.17/lb to convert nickel concentrate to a nickel powder, the C1 cash cost of producing nickel powder would be $1.25/lb of nickel. Talon is working towards developing a flowsheet to determine the cost of converting nickel concentrates to nickel powder at the mine site.

AISC: The AISC of producing a pound of nickel in concentrate sold FOB at the mine gate is the C1 cash cost plus royalties and sustaining CAPEX as shown in the following table.

Table 12: AISC of the Nickel Powder Scenario

| Cost | $/lb Ni in Concentrate |

| C1 Cash Cost | $0.08 |

| Government and Private Royalties | $0.62 |

| Sustaining CAPEX | $0.37 |

| AISC of Producing Nickel in Concentrate at the Mine Gate | $1.07 |

In the Nickel Powder Scenario, nickel concentrates are sold at a discount to the LME nickel price, similar to the Nickel Concentrate Scenario. However, the discount to the LME nickel price is expected to be smaller for the Nickel Powder Scenario as compared to the Nickel Concentrate Scenario, given the supply chain from mine to battery removes several processing and transportation steps (thereby creating a win-win for both the mining company and the battery company).

Should the facility that converts nickel concentrates to nickel powders for the EV industry be co-located at the mine site, transportation costs will be extremely low compared to the Nickel Concentrate Scenario: Nickel powders for the EV industry require 99.99%+ purity and therefore, almost no waste is transported. In contrast, nickel concentrates at approximately 11% by mass of valuable metals requires the transportation of 89% waste. As with the Nickel Sulphate Scenario, the product under the Nickel Powder Scenario is sold FOB at the mine gate.

Nickel concentrates need to be refined to produce nickel powder for the EV market, which will require additional capital and operating cost: For instance, if it costs $1.17/lb to convert nickel concentrate to a nickel powder, the AISC of producing nickel powder would be $2.24/lb of nickel. Talon is working towards developing a flowsheet to determine the actual cost of converting nickel concentrates to nickel powder at the mine site.

B) Nickel Sulphate Scenario

Nickel sulphates produced at site will be sold FOB at the mine gate and therefore, the C1 cash cost is calculated as shown in the following table:

Table 13: C1 Cash Cost of the Nickel Sulphate Scenario

| Cost | $/lb Ni in Ni Sulphates |

| On-site Cash Costs | $2.05 |

| On-site Cost of Converting a Nickel Concentrate to a Nickel Sulphate | $1.16 |

| Off-site Costs of By-products | $0.23 |

| Less: By-product Revenue | ($2.42) |

| Net Cost of Producing Nickel in Nickel Sulphates at the Mine Gate | $1.02 |

On site cash costs are higher for the Nickel Sulphate Scenario (before accounting for the cost of converting nickel concentrate to a nickel sulphate), as 95% of nickel in concentrates is expected to be recovered in the hydrometallurgical process, thereby reducing the denominator (pounds of nickel shipped) and increasing the overall cost per pound of nickel.

The higher by-product revenue compared to the Nickel Powder Scenario is due to higher cobalt revenues, as the Nickel Sulphate Scenario produces a cobalt sulphide, which due to its grade has high payabilities (compared to the lower payabilities assumed in the Nickel Powder Scenario).

AISC for nickel sulphates produced at site is calculated as shown in the following table:

Table 14: AISC of the Nickel Sulphate Scenario

| Cost | $/lb Ni in Ni Sulphates |

| C1 Cash Cost | $1.02 |

| Government and Private Royalties | $0.78 |

| Sustaining CAPEX | $0.51 |

| AISC of Producing Nickel in Nickel Sulphates at the Mine Gate | $2.31 |

In the Nickel Sulphate Scenario, nickel sulphates are sold as opposed to nickel concentrates. The traditional supply chain requires the production of LME grade nickel that is used as a feedstock to produce nickel sulphates. Nickel sulphates are therefore typically sold at a premium to the LME nickel price. In the case of the Tamarack Nickel Project, nickel sulphates could be produced directly from nickel concentrates at site, thereby reducing the number of process and transportation steps. The premium to market price applies irrespective of processing route.

Royalties per pound are higher in the Nickel Sulphate Scenario compared to the Nickel Powder Scenario because under the Nickel Sulphate Scenario, a value-added product (that results in a premium price) is sold.

AISC under the Nickel Sulphate Scenario is higher than the Nickel Concentrate Scenario because of the incremental CAPEX associated with the hydrometallurgical refinery.

C) Nickel Concentrate Scenario

The Nickel Concentrate Scenario contemplates the traditional nickel-to-stainless steel supply chain.

C1 Cost: The cost of producing a pound of nickel in concentrate sold CIF to the smelter less all by-product credits is shown in the following table:

Table 15: C1 Cost of the Nickel Concentrate Scenario

| Cost | $/lb Ni in Concentrate |

| On-site Cash Costs | $1.91 |

| Less: Value of By-products in Concentrate | ($2.95) |

| Net Cost of Producing Nickel in Concentrate at the Mine Gate | ($1.03)* |

| Product Handling, Transportation, Insurance and Losses | $0.43 |

| Smelting, Refining and Deductions by the Smelter/Refiner | $2.66 |

| C1 Cost of a lb of Nickel in LME Grade Briquettes | $2.05* |

*Does not total due to rounding

Under the Nickel Concentrate Scenario, by-product revenue is the highest because the by-products are calculated using the gross value of metal in the concentrate transported to the smelter.

Product handling, transportation insurance and losses in the Nickel Concentrate Scenario are high because of the need to transport both the nickel and copper concentrates from the mine to smelters.

The smelting, refining and deductions line item consists of both cash charges by the smelters/refiners such as treatment charges and refining charges as well as deduction of metal units sent to the smelter but not paid to the mine.

AISC: The AISC of producing a pound of nickel in concentrate sold CIF to the smelter less all by-product credits less all sustaining capital.

Table 16: AISC of the Nickel Concentrate Scenario

| Cost | $/lb Ni in Concentrate |

| C1 Cost | $2.05 |

| Government and Private Royalties | $0.59 |

| Sustaining CAPEX | $0.37 |

| AISC of a lb of Nickel in LME grade briquettes | $3.01 |

In the Nickel Concentrate Scenario, nickel concentrates are sold at a discount to the LME nickel price. This discount to the LME nickel price is expected to be higher for the Nickel Concentrate Scenario compared to the Nickel Powder Scenario, as the traditional supply chain from mine to stainless steel requires more processing and transportation steps. Traditionally, transportation and insurance costs are incurred by the mining company and is therefore included in the cost calculation.

The C1 cost of $2.05/lb nickel to produce a nickel briquette calculated for the February 2021 PEA is lower than the C1 cost of $2.67/lb Ni in the prior March 2020 PEA. By way of explanation, although there was an initial cost increase due to the addition of lower grade disseminated sulphide materials to the mine plan from both the 138 and USMSU Domains, this cost increase was more than offset by the reduction in costs due to economies of scale realized from increasing the production rate from 2,000 tpd to 3,600 tpd, as well as major improvements to mine access, development and stoping costs and the application of the latest publicly available smelting and refining terms, which have improved since the March 2020 PEA. In total, this resulted in a C1 cost reduction.

Similarly, the AISC of $3.01/lb nickel to produce a nickel briquette calculated for the February 2021 PEA is lower than the AISC of $3.57/lb Ni in the prior March 2020 PEA: royalties have decreased because of the inclusion of lower grade material in the mine plan and sustaining CAPEX on a per lb basis has increased.

Economic Analysis

At the assumed base case metal prices, key metrics of the February 2021 PEA of the Tamarack North Project are summarized in the following table.

Table 17: Key Metrics of February 2021 PEA

| All amounts in United States dollars |

February 2021 PEA | ||

| NICKEL POWDER SCENARIO | NICKEL SULPHATE SCENARIO | NICKEL CONCENTRATE SCENARIO | |

| After-Tax NPV(1), (2) | $567 million | $569 million | $520 million |

| After-Tax IRR(1) | 48.3% | 31.9% | 45.6% |

| Initial CAPEX and Working Capital | $316 million | $553 million | $316 million |

| Payback Period, pre-tax(3) | 1.4 years | 1.8 years | 1.4 years |

| Payback Period, after-tax(3) | 1.5 years | 2.1 years | 1.6 years |

| Mine Life(3) | 9 years | 9 years | 9 years |

(1) Metal prices of $8.00/lb Ni, $3.00/lb Cu, $25.00/lb Co, $1,000/oz Pt, $1,000/oz Pd and $1,300/oz Au.

(2) Discount rate of 7%. NPV calculated from the start of construction.

(3) From the start of production

Metal prices used for the base case financial evaluation, as well as for sensitivity cases, are summarized in the following table. Base case prices were based on analyst consensus long-term prices. "Low" was used to estimate a pessimistic scenario. Incentive pricing is based on an estimated price required to incentivize the construction of new mines to meet the projected increased demand for battery metals such as nickel and cobalt during the next decade.

Table 18: Assumed Metal Prices

| Unit | Low | Base Case | Incentive Pricing | |

| Ni | US$/lb | $6.75 | $8.00 | $9.50 |

| Cu | US$/lb | $2.75 | $3.00 | $3.50 |

| Co | US$/lb | $15.00 | $25.00 | $35.00 |

| Pt | US$/oz | $1,000 | $1,000 | $1,000 |

| Pd | US$/oz | $1,000 | $1,000 | $1,000 |

| Au | US$/oz | $1,300 | $1,300 | $1,300 |

Pre-tax and after-tax NPV at various discount rates, pre-tax and after-tax IRR, EBITDA and EBIT margin over the life of mine, and payback period from start of production in years for the three metal price cases (Low, Base Case and Incentive Pricing) are summarized in the following table.

Table 19: After-tax and Pre-tax NPV, After-tax and Pre-tax IRR, EBITDA and EBIT Margin over Life of Mine and Payback Period Using Low, Base Case and Incentive Metal Price Assumptions

| Nickel Powder Scenario | Nickel Sulphate Scenario | Nickel Concentrate Scenario | ||||||||

| Discount rate | Metal Price Case | Metal Price Case | Metal Price Case | |||||||

| Low | Base | Incentive | Low | Base | Incentive | Low | Base | Incentive | ||

| Pre-tax NPV | 7% | 496 | 688 | 917 | 478 | 711 | 970 | 439 | 629 | 854 |

| US$ millions | 8% | 463 | 646 | 863 | 438 | 660 | 906 | 409 | 589 | 803 |

| 10% | 404 | 570 | 767 | 367 | 568 | 790 | 355 | 518 | 712 | |

| Pre-tax IRR | 45.0% | 56.0% | 67.4% | 29.2% | 37.6% | 45.7% | 41.5% | 52.6% | 64.2% | |

| After-tax NPV | 7% | 415 | 567 | 744 | 387 | 569 | 769 | 369 | 520 | 695 |

| US$ millions | 8% | 386 | 530 | 698 | 351 | 524 | 714 | 342 | 485 | 651 |

| 10% | 333 | 463 | 616 | 286 | 443 | 615 | 293 | 423 | 573 | |

| After-tax IRR | 39.3% | 48.3% | 57.7% | 25.1% | 31.9% | 38.6% | 36.4% | 45.6% | 55.1% | |

| EBITDA margin | 64% | 68% | 70% | 60% | 64% | 66% | 60% | 64% | 67% | |

| EBIT margin | 43% | 50% | 55% | 34% | 41% | 47% | 39% | 46% | 52% | |

| Payback from start of production (pre-tax, undiscounted) | ||||||||||

| 1.6 | 1.4 | 1.2 | 2.2 | 1.8 | 1.6 | 1.7 | 1.4 | 1.2 | ||

| Payback from start of production (after-tax, undiscounted) | ||||||||||

| 1.8 | 1.5 | 1.3 | 2.4 | 2.1 | 1.8 | 1.9 | 1.6 | 1.4 | ||

Recommendations

It was previously recommended that Talon should determine whether it should sell nickel concentrates or nickel sulphates by developing and contrasting the economic impact of these two scenarios. The Company's targeted completion date to achieve this milestone was at the end of February 2021.

Talon has now achieved this objective.

Since that time, Tesla, Inc. has articulated that it has the goal of consuming raw nickel powder, which will dramatically simplify the nickel to battery supply chain. Talon's nickel powder scenario contemplated in the February 2021 PEA is based on selling nickel concentrates to a co-located refinery that produces high purity nickel powders. Talon believes, however, that the same refinery could potentially produce high purity iron powders as a by-product. It is therefore recommended that going forward, the economic impact of a scenario where Talon produces both refined nickel and iron powders is quantified.

If successful, Talon could potentially produce three products:

-

Refined nickel powders for the nickel battery cathode market;

-

Refined iron powders for the lithium iron phosphate (LFP) market; and

-

Copper concentrates.

Talon's next milestone should therefore be to develop a flowsheet in addition to CAPEX and OPEX estimates for the above scenario. A successful outcome could allow Talon to lower its cut-off grade and therefore, increase the amount of metal it could produce from the Tamarack Nickel Project. This, in turn, would lead to a different resource envelope and consequently, mine plan.

Once Talon has decided whether it should produce nickel concentrates, nickel sulphates or nickel and iron powders, the Company will complete a prefeasibility study.

In the meantime, going forward Talon should focus on resource expansion and definition drilling in order to progress towards prefeasibility and feasibility studies assuming the Company proceeds with the Nickel Powder Scenario contemplated in the February 2021 PEA. It is estimated that between 25,000 and 30,000 meters of drilling will be required, mostly focussed on expansion of the Tamarack Nickel Project's current resource area. Talon's in-house team of experienced specialists operate their own drilling and geophysical equipment efficiently and at low cost. It is therefore expected that this recommendation is achievable during 2021.

Talon also has a comprehensive geotechnical logging program in place and should therefore continue with laboratory testing of drill core, collecting down hole data using acoustic televiewer and full wave sonic technology, as well as in-situ stress measurement testing. Hydrological work should be conducted as appropriate for each level of study. Installation of multilevel vibrating wire piezometers in selected historical drill holes and additional aquifer property testing within the glacial till and bedrock aquifers are also recommended.

Geo-metallurgical testing programs should continue and should be based on the predicted Life-of-Mine feed bearing in mind the specific requirements of each of the possible customers for the different products listed above. It is recommended that Talon maintains optionality and complete the second phase of hydrometallurgical testing to produce nickel sulphates. Waste products from geo-metallurgical testing programs should be used to continue environmental test work.

Conclusions

The February 2021 PEA illustrates a high after-tax IRR, low All-in Sustaining Cost (AISC), low capital intensity and a quick payback for the Tamarack Nickel Project. The February 2021 PEA also clearly demonstrates that the Tamarack Nickel Project has the optionality to produce either nickel sulphates or nickel concentrates for refined nickel powders to be used for the EV market or nickel concentrates for the stainless steel market, with all contemplated scenarios having extremely robust economics.

As discussed, the February 2021 PEA does not include any of the Company's recent positive drilling results both within the Tamarack Nickel Project's current resource area (see the Company's press releases dated January 12, 2021 and January 26, 2021) and approximately 350 meters up-dip to the north-east of the Tamarack Nickel Project's current resource area (i.e., drill results from the area known as CGO East, as discussed in the Company's press releases dated September 16, 2020 and November 2, 2020).

The February 2021 PEA will be filed on SEDAR (www.sedar.com) and on the Company's website (www.talonmetals.com) within 45 days.

Quality Assurance, Quality Control and Qualified Persons

For the purposes of the February 2021 PEA and this press release, the Qualified Persons ("QP"), as such term is defined in NI 43-101 are as follows:

The mineral resource estimate contained in this news release was prepared by or under the supervision of Mr. Brian Thomas (P.Geo.), who is a geologist independent of Talon and an employee of Golder Associates Ltd. In addition, Mr. Thomas has reviewed the sampling, analytical and test data underlying such information and has visited the site and reviewed and verified the QA/QC procedures used at the Tamarack North Project and found them to be consistent with industry standards. In Golder's opinion, the mineral resource estimate disclosed herein has been prepared in accordance with CIM best practice guidelines.

The overall February 2021 PEA NI 43-101 report was compiled (with inputs from other QPs as indicated) by Mr. Tim Fletcher, P. Eng., a Senior Project Manager with DRA Americas who is independent of the Company.

The mining methods, including mine development and mine plan, were developed by Mr. Andre-Francois Gravel, P. Eng., a Senior Mining Engineer with DRA Americas who is independent of the Company.

The mine CAPEX and OPEX were developed by Mr. Daniel M. Gagnon, P. Eng., a Senior Mining Engineer and VP Mining and Geology for DRA Americas who is independent of the Company and who has visited the site.

A summary of metallurgical test work and proposed mineralized and hydrometallurgical processing methods for the project were compiled by Mr. Oliver Peters, P. Eng., Principal Metallurgist and President of Metpro who is independent of the Company.

Proposed hydrometallurgical processing methods for the project were reviewed by Dr. Volodymyr Liskovych, PhD, P Eng., a Principal Process Engineer with DRA Americas, who is independent of the Company.

The economic analysis, including pre-tax and after-tax financial results and sensitivity analysis was completed by Mr. Christian Hizmeri, MBA, Financial Analyst for DRA Americas (under the supervision of Mr. Daniel M. Gagnon, P. Eng.) who are both independent of the Company.

The conceptual design of the CFTF was completed by Mr. David Ritchie, P.Eng., Engineering Manager with SLR Consulting (Canada) Ltd. who is independent of the Company.

The requirements for the backfill paste recipe and underground distribution methodology were reviewed by Mr. Leslie Correia, Pr. Eng., Engineering Manager for Paterson & Cooke Canada Inc., who is independent of the Company.

Environmental considerations and permitting were addressed by Ms. Andrea Martin, P.E., Foth Infrastructure & Environment, LLC, De Pere Wisconsin, who has reviewed and verified detailed environmental study requirements used by Talon for the Tamarack North Project and found them to be consistent with industry standards. She is independent of the Company and has visited the site.

About Talon

Talon is a TSX-listed base metals company in a joint venture with Rio Tinto on the high-grade Tamarack Nickel-Copper-Cobalt Project located in Minnesota, USA, which comprises the Tamarack North Project and the Tamarack South Project. Talon has an earn-in to acquire up to 60% of the Tamarack Nickel Project. The Tamarack Nickel Project comprises a large land position (18km of strike length) with numerous high-grade intercepts outside the current resource area. Talon is focused on expanding its current high-grade nickel mineralization resource prepared in accordance with NI 43-101; identifying additional high-grade nickel mineralization; and developing a process to potentially produce nickel sulphates responsibly for batteries for the electric vehicles industry. Talon has a well-qualified exploration and mine management team with extensive experience in project management.

For additional information on Talon, please visit the Company's website at www.talonmetals.com or contact:

Sean Werger, President

Email: This email address is being protected from spambots. You need JavaScript enabled to view it.

Telephone: 416-361-9636

Forward-Looking Statements

This news release contains certain "forward-looking statements". All statements, other than statements of historical fact that address activities, events or developments that the Company believes, expects or anticipates will or may occur in the future are forward-looking statements. These forward-looking statements reflect the current expectations or beliefs of the Company based on information currently available to the Company. Such forward-looking statements include, among other things, statements relating to the results of the February 2021 PEA, including with respect to estimates of mineral resource quantities and qualities, the mining method, mine life, the basis of design of the February 2021 PEA, optionality, capital and operating costs, NPV (and future increases to NPV), IRR, EBITDA, EBIT, payback, cash costs (C1 cash cost and AISC), targets, goals, objectives and plans, including statements relating to the timing, results and costs of future exploration, including resource expansion, geophysical potential and results, and drilling plans, quantification of producing both refined nickel and iron powders, and assumptions in respect of metal pricing, future news and future studies, including a prefeasibility study and feasibility study.

Forward-looking statements are subject to significant risks and uncertainties and other factors that could cause the actual results to differ materially from those discussed in the forward-looking statements, and even if such actual results are realized or substantially realized, there can be no assurance that they will have the expected consequences to, or effects on the Company. Factors that could cause actual results or events to differ materially from current expectations include, but are not limited to: failure to establish estimated mineral resources, the grade, quality and recovery of mineral resources varying from estimates, the uncertainties involved in interpreting drilling results and other geological data, inaccurate geological and metallurgical assumptions, including with respect to the size, grade and recoverability of mineral reserves and resources, uncertainties relating to the financing needed to further explore and develop the properties or to put a mine into production and other factors including exploration, development and operating risks, uncertainties with economic estimates, capital and operating costs, mine plan and development issues.

Any forward-looking statement speaks only as of the date on which it is made and, except as may be required by applicable securities laws, the Company disclaims any intent or obligation to update any forward-looking statement, whether as a result of new information, future events or results or otherwise. Although the Company believes that the assumptions inherent in the forward-looking statements are reasonable, forward-looking statements are not guarantees of future performance and accordingly undue reliance should not be put on such statements due to the inherent uncertainty therein.

The mineral resource figures disclosed in this news release are estimates and no assurances can be given that the indicated levels of nickel, copper, cobalt, platinum, palladium and gold will be produced. Such estimates are expressions of judgment based on knowledge, mining experience, analysis of drilling results and industry practices. Valid estimates made at a given time may significantly change when new information becomes available. While the Company believes that the resource estimates disclosed in this news release are accurate, by their nature resource estimates are imprecise and depend, to a certain extent, upon statistical inferences which may ultimately prove unreliable. If such estimates are inaccurate or are reduced in the future, this could have a material adverse impact on the Company.

Mineral resources are not mineral reserves and do not have demonstrated economic viability. Inferred mineral resources are estimated on limited information not sufficient to verify geological and grade continuity or to allow technical and economic parameters to be applied. Inferred mineral resources are too speculative geologically to have economic considerations applied to them to enable them to be categorized as mineral reserves. There is no certainty that mineral resources can be upgraded to mineral reserves through continued exploration.